Disputes are Weighing Heavy on Your Business

Let our proactive platform take chargebacks off your shoulders

Let's connect

Transaction disputes are one of the worst things a merchant can face when trying to build a solid business. These claims are not only tiring and frustrating to manage but can also be very costly. Not all claims are legitimate, which makes the whole phenomenon even more tricky to deal with. It’s essential to understand what transaction disputes are, so you can handle them if push comes to shove. Let’s take a look at what these transaction disputes are, why they are made, and what you can do about them.

Table of Contents

When a customer purchases something from you, they can later get in touch with their bank and demand their money back. This is essentially what a transaction dispute is. Customers can initiate it by contacting their bank and telling them they did not authorize one of the transactions on their card.

One important thing to note is that transaction disputes are not the same thing as a chargeback. They are the first step in initiating a chargeback, though. If a claim is made and the issuing bank deems it acceptable, it turns into a chargeback.

There can be many reasons for a customer to dispute one or more of their transactions. Here are some:

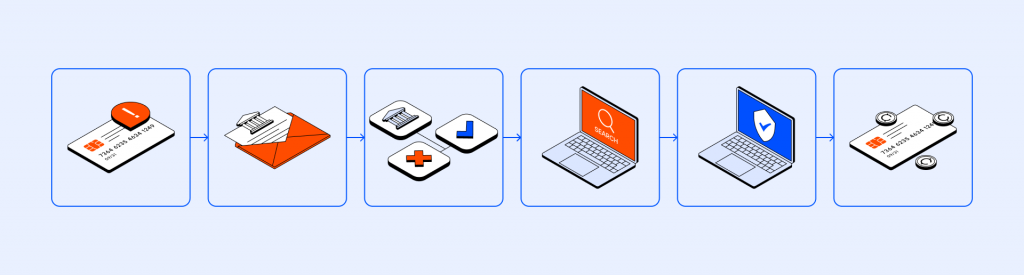

If you want to know how transaction disputes work, here are the basic steps of the process that you should be aware of:

How long transaction disputes take depends on some factors like who the merchant is and what kind of claim is made. Usually, when a customer makes a dispute, you have 7 days to respond to the issuing bank about whether you accept it or want to fight it. After that, the chargeback process begins, which takes a much longer time.

Overall, the whole transaction disputes process can take up to 90 days if the payment was made with a debit card and up to 60 days if it was made with a credit card. If the customer decides to contact you directly about their problem, you may be able to come to an agreement and end the problem in a few days.

There are a number of problems with the transaction disputes process. Here are some:

Here are some tips you can use to start managing transaction disputes and hopefully maintaining your company’s ROI in the process:

These simple steps can help you not only in managing transaction disputes once they arise but also in preventing them from ever taking place at all.

Many cardholders abuse this process, as committing fraud is very easy this way. Here are some ways in which customers abuse the process:

Chase transaction disputes work the same way as with most other banks. First, the bank suggests that customers review the details of the charge they have an issue with. It allows them to access these details and then suggests that they contact the merchant directly first.

The good thing about Chase transaction disputes is that the bank tries to educate its users about what they should do before contacting the bank, trying to resolve the issue with the merchant, as that can be done in just a few days.

Transaction disputes and chargebacks are related but refer to different stages and processes in the resolution of payment-related issues. A transaction dispute occurs when a customer raises a concern or disagreement regarding a specific transaction with a merchant. This can include issues such as billing errors, incorrect amounts charged, defective products, delivery problems, or unauthorized transactions.

A chargeback is a formal dispute initiated by the customer with their bank or card issuer. It typically occurs after a transaction dispute has been escalated, and the customer’s concerns were not satisfactorily addressed. The bank or card issuer investigates the claim, collects evidence from both parties (merchant and customer), and makes a decision regarding the validity of the dispute. If the chargeback is deemed valid, the funds are reversed from the merchant’s account and returned to the customer.

Banks reserve the right to reject a cardholder’s dispute. The most common reasons banks reject cardholders’ disputes include:

Specific policies and procedures for dispute resolution may vary among banks and card issuers. Cardholders should familiarize themselves with the terms and conditions of their credit cards and provide accurate and detailed information when filing a dispute to ensure a fair evaluation by the bank.

Merchants make several mistakes during transaction disputes that hinder their ability to successfully resolve the issue. Here are the most common mistakes and some tips to help merchants reduce their chance of being involved in transaction disputes:

To avoid transaction disputes, merchants should take these proactive steps:

To save your ROI and reputation, you can get in touch with us and see how Chargebackhit can help in your case. We are a reputable company that offers chargeback prevention and resolution services to merchants. We offer highly useful alerts to merchants when a customer disputes a transaction, by using both Verifi and Ethoca networks.

This helps businesses resolve the issue directly with their customer rather than having to go through the whole chargeback process. Chargebackhit also helps merchants win such cases by automatic resolution, so you don’t have to worry about pretty much anything.

In the case of friendly fraud, Chargebackhit is equipped to fight for reclaiming your revenue as well. So, the company offers a complete package of services to its users, from prevention to resolution. And all through the process, you as the merchant do not have to worry too much and can dedicate yourself to your business instead.

Let our proactive platform take chargebacks off your shoulders

Let's connectUsing our direct connection to Visa, Mastercard, and issuing banks, we assist merchants on the very first stages of the dispute-resolution process.

By clicking “Get Started,” you agree to our Privacy Policy

Thank you for something

We will contact you shortly. If you have any further questions, please contact us at support@chargebackhit.com.

Thank you

We've sent the whitepaper to your email.

Thank you

We will contact you shortly. If you have any further questions, please contact us at support@chargebackhit.com.

Thank you

We will contact you shortly. If you have any further questions, please contact us at support@chargebackhit.com.

Thank you

We will contact you shortly. If you have any further questions, please contact us at support@chargebackhit.com.